HIGHLIGHTS

- Strong Sales growth of 5.5% in 3Q16 despite the sluggish retail market.

- Store expansion continues, 2057 stores as at end Sept 2016

Gross profit margin continues to improve versus last year. - Significant negative impact on 3Q 16 profit from the increase in Minimum Wage from 1st July 2016.

- Average spend per customer increase of approx. 4% in 3Q 2016 versus same period last year.

Comments from CEO – GARY BROWN

“The 3rd Quarter 2016 continues to highlight the tough retail market in which we operate since the introduction of GST coupled with low consumer sentiment and spending. The impact of the Minimum Wage increase in July 2016 has negatively impacted the 3Q16 results. We remain confident that continuous store expansion, refurbishment, promotional activity, improved merchandise mix and expanded in-store services will continue to deliver positive results despite the challenging headwinds.”

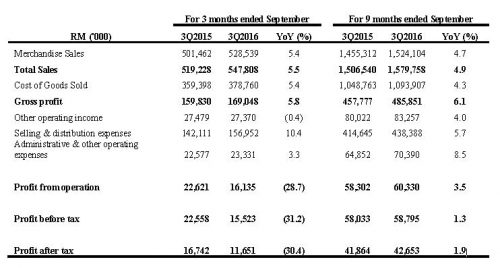

For the 3rd Quarter ended 30 September 2016

The Group’s revenue for the current quarter of RM547.8 million grew by RM28.5 million or 5.5% against the corresponding quarter’s revenue in the previous year of RM519.2 million. The growth in revenue continued to be driven by the growth in new stores, improved merchandise mix and consumer promotion activity. This growth was achieved despite prolonged on-going retail market softness caused by weak consumer confidence/spending.

Gross profit of RM169.0 million improved by RM9.2 million or 5.8% compared to the corresponding quarter in the previous year and this was mainly attributed to the revenue growth of 5.5%.

Selling and distribution expenses for the quarter increased by RM14.8 million or 10.4%, mainly caused by new store expansion resulting in higher staff cost, rental cost, store depreciation expense and utility cost. In addition, the increase in the minimum wage effective 1st July 2016 has caused the store staff costs to rise by approximately 10% in the current quarter.

Administrative and other operating expenses for the quarter increased by RM0.7 million or 3.3% due to higher staff cost, head office IT depreciation expense and amortization of intangible assets.

The profit before tax of RM15.5 million decreased by RM7.0 million or 31.2% compared to the corresponding quarter in 2015 despite positive sales growth due to higher selling and distribution expenses caused by new store expansion and the impact of minimum wage increase effective 1st July 2016.

For the 9 months ended 30 September 2016

For the 9 months ended 30 September 2016, the Group’s revenue of RM1.58 billion grew RM73.2 million or 4.9% against the corresponding 9 months’ revenue in the previous year of RM1.51 billion. The growth in revenue was driven by the growth in new stores (total stores as at 30 September 2016: 2,057 stores), improved merchandise mix and consumer promotion activity.

Gross profit improved by RM28.1 mil or 6.1% compared to the corresponding 9 months in the previous year and this was mainly attributed to the revenue growth of 4.9% and gross profit margin expansion of 0.4% points.

Selling and distribution expenses for the 9 months period in 2016 increased by RM23.7 million or 5.7%, mainly caused by higher staff cost, rental cost, store depreciation expense and utility cost which is in tandem with new store expansion coupled with impact of minimum wage increase on the staff cost.

Administrative and other operating expenses decreased by RM5.5 million or 8.5% vis-à-vis the corresponding 9 months in the previous year due to higher staff cost, head office IT depreciation expense and amortization of intangible assets.

The profit before tax of RM58.8 million increased by 1.3% or RM0.8 million despite revenue growth of 4.9% and gross margin expansion by 0.4% points due to higher selling and distribution expenses from new store expansion and also the impact of minimum wage increase effective 1 July 2016 on the salary cost.

Future Prospects

The Board of Directors is of the view that the trading conditions for the remaining period of the current financial year is expected to remain challenging due to continued weak consumer confidence/spending and current macro-economic conditions. Despite this latest development, we remain positive of holding onto our market leading position.

{kind=link}