Companies are know to change their corporate names after scandals partly as a way to bury the past and move forward. In China, the latest company to join the list is Prince Frog International Holdings.

Prince Frog, a Hong Kong-listed, China-based children care products and adult care products maker, was accused of accounting fraud by Glaucus Research in October 2013. The short-seller alleged Prince Frog had overstated sales of its signature moisturizing lotions based on an analysis of Nielsen data.

Prince Frog was able to resume trading after its shares were suspended for more than one month after giving a comprehensive reply refuting the allegations. On 7 April 2014, Prince Frog is no longer the fairy tale frog as the name will be changed to something more generic – China Child Care Corporation Limited. The reason given was to reflect the “diversified brand offerings of babies’ and children’s personal care products.” But for the informed outsiders, the name change seems like a move by the management to forget about the Glaucus saga and move on to a new chapter.

Made-in-China products have flooded the world and it is hard to live a normal life without made-in-China products. Even Chinese home grown burger chains are heading overseas. After years of being overshadowed by the likes of KFCs and McDonald’s, homegrown burger chains have grown in scale and have reached a point where they are starting to export their fried chicken to the world.

At the end of 2013, Yum! Brands operated 4,600 KFCs and 1,264 Pizza Huts in China, making it the largest western fast food chain in the country. Taiwan’s Dico’s had over 2,000 outlets at the end of 2013, while McDonald’s will open its 2,000th outlet by the end of April 2014.

Unknown to the outside world and oblivious to some ordinary urban Chinese consumers, CNHLS (Hualaishi 华莱士) is actually the second largest western fast food chain in China after KFC by store count with about 4,800 stores mainly in lower tier cities. Following the footsteps of CNHLS are a legion of equivalently aggressive local western fast food chains with funny abbreviated names like LEM (乐而美), KDS (快乐星)and Pala (派乐). LEM and Pala each has over 1,000 stores. They expand mainly through franchising without significant investment on their own.

LEM and KDS are the more aggressive ones internationally. KDS said it is making inroad into Myanmar and Africa since 2011, while LEM opened its first outlet in South Africa in February 2014. It makes sense for China’s western fast food chains to enter developing and less developed markets as consumers there may not even have tasted McDonald’s or KFC such as the case with Myanmar. As long as there is fried chicken and fried food selling at affordable prices, Chinese western fast food chains will be in a good position to tap such demand.

Alfamart is expected to debut in the Philippines soon as it has already started the hiring process. It has been a belated development as the company said in November 2013 that it expected to open the first Alfamart store in the Philippines in the first quarter of 2014. The company has since missed the first quarter “deadline.”

Alfamart Trading Phils Inc is hiring through Best Jobs Philippines (http://www.bestjobsph.com), one of the most popular job sites in the country.

The company needs:

1.) AutoCAD operators

2.) Male/female store crew

3.) Location coordinators/surveyors etc

Essentially, the company needs all the manpower to run a chain of minimart. What is interesting is Alfamart needs them in Cavite province, which lies in the southern shores of Manila Bay next to Metro Manila and Laguna. Crew is also needed in Las Pinas in the southern tip of Metro Manila. In Cavite, the stores will be launched in the Cavite provincial capital Imus and in Dasmariñas. The crew will be paid the minimum wage.

In Cavite, the daily minimum wage is about PHP 250 (USD 5.57) (retail and service establishments employing not more than 10 workers) or PHP 349.50 (non-agriculture). See link.

The focus on Cavite and Las Pinas shows Alfamart is targeting the outlying areas first in a classic “surrounding the cities from the countryside (in this case lower tier cities)”. This approach gives Alfamart a lower cost structure as the minimum wage in Metro Manila is higher at PHP 466 for non-agriculture and PHP 429 in retail and service establishments employing not more than 10 workers. Alfamart is already facing pressure from rising labour cost in its home market in Indonesia. As it moves into the Philippines, Alfamart will surely focus on reducing labour cost to the minimum as salary forms a significant component of the cost structure in the minimart business.

PT Sumber Alfaria Trijaya (Alfamart), the operator of the Alfamart minimart chain in Indonesia, is reeling under labour cost pressure. High inflation and fuel costs, which rose by 44% for petrol and 22% for diesel in 2013 had pushed about 2 million workers across the county to go on strike in October 2013 to demand for higher wages. To mitigate the effect of higher cost of living, the authorities implemented drastic wage hike in 2013 with a 44% increase in the minimum wage in Jakarta to IDR2.2 million (USD228). The wage increase varies by regions. In East Kalimantan, the wage hike was 49% but only 11% in Aceh.

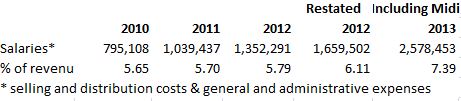

The sharp rise in salary has hit retailers hard. Alfamart saw a sharp 50% spike in selling and distribution expenses in 2013 versus 2012. The growth in selling and distribution expenses was offset by a slower but strong growth in gross profit, up 45.6% over 2012. The result was the deterioration of net profit margin, down 0.4 percentage points to 1.7% (before taking into account the incorporation of PT Midi Utama Indonesia) or a 0.14 percentage fall (after restatement of the 2013 results to take into account PT Midi Utama).

In 2013, Alfamart upped its stake in PT Midi Utama Indonesia, the operator of Alfa Midi mini supermarket, Alfaexpress convenience store and Lawson convenience store, to 56.72% from 12.75% in 2012.

As a % proportion of total revenue, 2008-2013 (note 2012-2013 figures do no take into account the investment in Midi Utama)

% of net sales

A closer look at the salary component of the cost structure shows a rise in the share of salary cost out of total revenue in 2013, rising from 6.11% in 2012 to 7.39% in 2013.

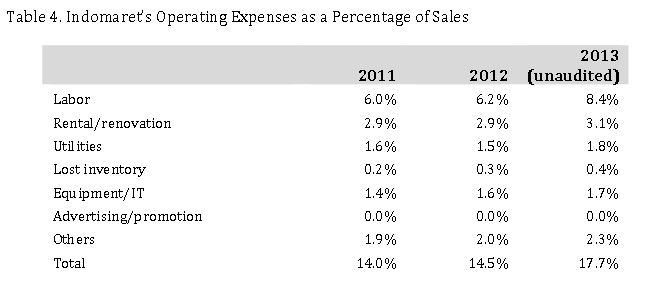

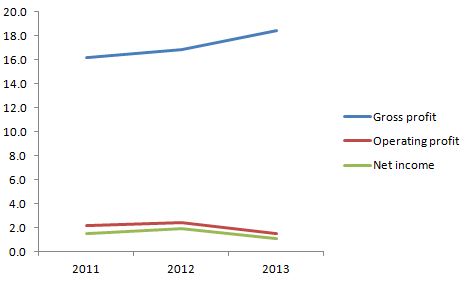

Such situation is an industry-wide problem, affecting not just Alfamart but also its key competitor Indomaret. According to PT Indoritel, labour operating expenses as a percentage of sales for Indomaret surged to 8.4% in 2013, a 2.2 percentage point increase. The result was a sharp decline in net profit margin to 1.1% in 2013 from 1.9% in 2012, translating into a 35.5% year-on-year fall in net profit to IDR372 billion.

From PT Indoritel Q4 Newsletter

From PT Indoritel Q4 Newsletter

Margin (%) – From PT Indoritel Q4 Newsletter

Cash Flow

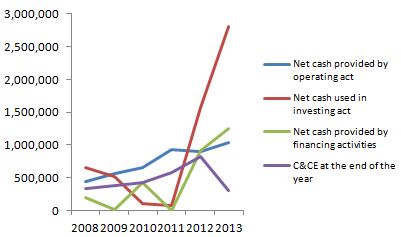

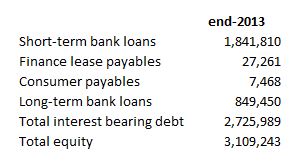

Alfamart is running out of cash as net cash used in investing activities has surged to an all time high of IDR 2.8 trillion in 2013 with acquisition of property, plant and equipment accounting for IDR1 trillion and long-term rent at IDR719 billion, up respectively from IDR907 billion and IDR591 billion in 2012. To sustain its capex needs, the company has issued new shares, raising IDR1.17 trillion in 2012 and raising short-term and long-term bank loans totaling IDR1.94 trillion in 2013. As a result of the rising indebtedness, finance costs (before including Midi Utama) escalated to IDR216 billion in 2013 from IDR46 billion a year ago.

Sumber Alfaria Trijaya cash flow, 2008-2013 (note 2012-2013 figures are not restated and does not take into account Midi Utama)

Sumber Afaria Trijaya

1,000 new stores planned in 2014

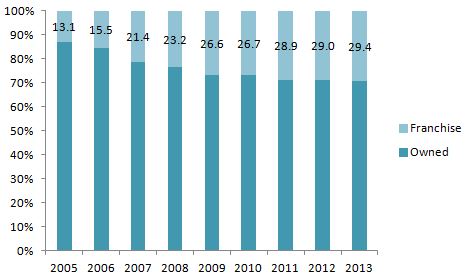

Alfamart is accelerating franchising to comply with government restriction on company-owned outlet under the New Franchise Law. Companies have five years from the announcement of the regulation in February 2013 to adjust. The regulation limits company-owned stores up to 250 units with the rest to be franchised. Judging by the current rate of conversion from company to franchise stores, Alfamart is not likely to meet the franchise target. Hampering such effort is an aggressive plans to open another 1,000 new outlets in 2014 focusing on areas outside of Java.

Sumber Alfaria Trijaya – breakdown by store format (%)

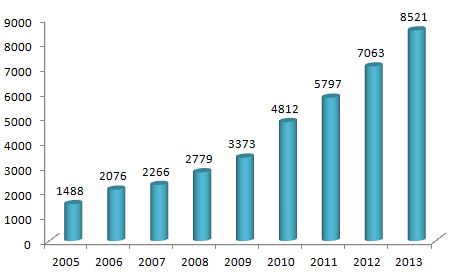

Sumber Alfaria Trijaya outlet – 2005-2013

Segment

By segment, food has the biggest share of net sales and gross profit as well as the highest gross profit margin.

Kellogg's and Campbell's "old" packaging - Image taken by the author

Packaged food companies are capitalising on the good ol’ days targeting teens and young consumers who think retro is hip and reconnect with the 40-50-year-olds. Kellogg’s and Campbell’s are the latest throwback products in Malaysia, both come in tin packaging. Retro marketing gives consumers the assurance of authenticity and simplicity.

Such marketing technique also reminds consumers of the history of the brand and how it has become part of the life of ordinary Malaysians for the past decades. The Jacob’s 60th anniversary packaging in 2013 commemorated the company’s first commitment that tracked back to 1953 to be the nutritious choices for all Malaysians.

Jacob’s retro tin (right) – Image taken by Mini Me Insights in Nov 2013

As more brands celebrate their anniversary, some of them may choose to become nostalgic adopter, reminding consumers of the brand’s heritage and longevity.

Pinnacle Foods (M) Sdn Bhd, formerly known as Pran Foods (M) Sdn Bhd, has introduced a differentiated product in the Malaysian juice category. The latest 125ml juice for kids has filled the void in the single-serve 125ml format. The smallest mainstream packaging size in the juice category at the moment is 250ml for both glass bottle and carton.

Dutch Lady Kid Full Cream Milk 4 x 125ml – Image from Tesco Malaysia

Similar 125ml format has already being adopted in the UHT milk category in Malaysia. Why a similar mini pack is not used by the juice category to target kids? A small pack size helps in portion control and fits nicely in the lunch box.

The Pran 125ml juice comes in fruit cocktail, mango and orange flavours and is selling for RM2.50 for 4x125ml at the Hero Supermarket in Taman Dagang, Selangor. Compared to Pran Junior Juice, the Marigold Fruit Drink Apple 6x250ml is selling for RM5.40. On a per volume basis, Marigold (RM3.6/L) is cheaper than Pran (RM5/L).

Getting Pran 125ml juices into more stores is the key challenge as I have only seen the Junior Juice at Hero Supermarket and not in the bigger outlets such as Tesco, Giant and Aeon Big. At the moment, Pran mango in PET bottles have entered Aeon Big. However, if one were to go to local Indian-owned grocery stores, there are more selection of Pran products, which is a strong indication that Pran goes for smaller grocery stores first before going into the bigger retail establishments.

“The real taste of mango” – Image taken by the author at Aeon Big

PT Mayora Indah Tbk (MYOR), known for its Kopiko coffee candy, is one of Indonesia’s biggest food companies. The company makes everything from coffee and cereal to candy and biscuits. Its revenue grew at a CAGR of 20.6% between 2008 and 2013, operating income up by a CAGR of 24.8% and net income rose by a CAGR of 32.1% over the six-year period.

MYOR yoy (%), 2009-2013

MYOR margin (%), 2008-2013

2011 was a terrible year for MYOR due to high commodities prices. During the first half of 2011, the cost of palm oil, sugar, wheat and coffee escalated. To keep its prices competitive, the company chose to absorb most of the raw material price hike to maintain the sales momentum. Nonetheless, COGS grew faster than revenue growth, which resulted in the decline in overall profitability. In 2012, the company imported 40% of its raw materials.

2012 was a strong recovery year for the company with net income surging by more than half. The following year 2013 bottom line was boosted by gains in foreign exchange of IDR308 billion (2012: IDR38 billion). The huge gains in foreign exchange has to do with the depreciation of the rupiah versus the greenback. MYOR may see a smaller gain on foreign exchange with the recovery of the rupiah against the US dollar in 2014. Therefore, net income may be affected.

Key concerns:

Labour cost

Proportion (%) of total net sales, 2008-2013

MYOR is facing rising labour cost pressure, which rose to 4.8% of total net sales in 2013, up by 1.8 percentage points from 2008. Indonesia’s minimum wage for 2014 grew by a range of 7.66% in East Kalimantan to 29.64% in Bangka Belitung with Jakarta up by 11%. See minimum wage.

Gearing level

The gearing ratio fell to 51.09% in 2013 from 79.77% in 2012 due to the increase in cash and cash equivalent, while total borrowing remained unchanged at IDR3.7 to IDR 3.8 trillion with most of them non-current liabilities with a repayment period of longer than one year. Interest expense has been manageable, thanks to rising sales. MYOR has been cutting back on capex to reduce its gearing level. Most of the expansion was made in 2012, which will be adequate for future needs.

Capex, 2009-2013

Sales breakdown by geography

Revenue breakdown by markets

MYOR has been aggressively expanding its global footprint. The export market will be the key driver for MYOR going forward. In Malaysia, MYOR has become very active in the market with innovative products such as the low acid coffee Kopiko LA Coffee and its biscuit ranges such as Astick and Slai O’lai. Malaysia is ripe for MYOR’s Energen Cereal as the country has a strong culture of drinking 3-in-1 cereals.

In China, its Astick stick biscuit has good shelf presence in the leading trade channels. As for the Kopiko candy, it is well known globally.

By segment

Revenue breakdown by product segments

Operating income breakdown by product segments

Food processing is proven to be a more lucrative business for MYOR and this is reflected in the higher share of food processing in operating income. MYOR is moving in the right direction by focusing more on food processing than on the highly competitive coffee business.

Conclusion

The growing export business and the focus on food processing put the company in a good position. The key risks are commodities prices and debt-fuelled expansion. The focus on one-off items such as gains on forex may not be sustainable.

With an EPS of IDR 1,165 in 2013 and the current share price of IDR30,000 (28 March 2014), the P/E of 25.75 makes the company cheap in the FMCG space in Indonesia.

For a novel product like fried ice cream (aiskrim goreng), consumer education through demonstration is the only way to convince and teach consumers about the proper way to prepare the fried ice cream. The ice cream has to be cold, taken straight from the freezer and the optimum frying period is 8 seconds only.

The following photos were taken at Aeon Supermarket, Cheras Selatan on 28 March 2014.

Nestle and Marigold are going for volume in the yogurt category in Malaysia. A simple solution to sell yogurt as a family pack is to bind them using a plastic sheet. Such low-cost solution allows Nestle and Marigold the flexibility to sell yogurt as a pack of six or individually. Most major brands have always been marketing yogurt in individual pack as reflected in the current individual cup packaging with spoon format.

Nestle multi-pack yogurt – Image by the author

The only exception to this is Fonterra’s Anlene and Fernleaf Calci-Yum, which is meant more for home consumption as they do not come with individual spoons and easy-to-carry pack.

Anlene Yogurt – image from Tesco Malaysia

Fernleaf Calci-Yum – image from Tesco Malaysia

The latest multi-pack development is positive for Nestle and Marigold as consumers are now encouraged to buy in bulk and to eat yogurt more frequently. Such multi-pack format can improve volume sales and increase consumption frequency.

Once manufacturers phase out individual pack, consumers will have no other choice but to go for multi-pack and this is what is happening in South Korea. Given the low yogurt consumption in Malaysia relative to South Korea, it will take some time for this to happen in Malaysia but Nestle and Marigold are moving in the right direction.

Yogurt all in multi-pack format in South Korea – image by the author

Tenwow International Holdings Ltd (Tenwow) 天喔集团 is a leading packaged food and beverage producer and one of the largest distributors of packaged food and beverages in China. Its shares are traded on HKEx under the ticker 1219. The company IPOed in September 2013 and raised HK$1.58 billion ($203 million) at the top of the range.

Latest financial results:

Tenwow has successfully put a lid on cost and good cost control has improved its bottom line, leading to steady improvement in all its key profit ratios. Gross profit margin in 2013 reached 15.6%, while net income margin improved to 6.1%. The low net income margin has been weighed down by the dependence on low-margin third party brand products. In 2013, the gross profit margin of third party brands stood at 10.2%, compared to 28% for own brands.

Tenwow yoy (%)

Tenwow margins (%)

Even though own brand’s share of revenue is rising, third party brands still have the largest share of revenue. As of 30 June 2013, Tenwow distributed over 4,300 different products of 76 international local brands. The brands include Dove confectionery, Glico snacks, Red Bull energy drink, Heinz baby food, Kraft snacks, Wrigley candy, Nestle sweets, Mars petfood, Unilever house care products, Wahaha beverage, Nestle coffee and Wang Lao Ji herbal tea. Alcoholic beverages include brands such as Remy Martin, Martell, Hennessy and Chivas Regal.

Revenue % split by third party and own brand products

Product segment:

Revenue mix (%), 2011-2013

The good thing about the business model of Tenwow is having the flexibility to adjust the product mix to improve margins. The share of alcoholic beverages by revenue is shrinking, while non-alcoholic beverages and food & snacks are rising. The decline in the revenue share of alcoholic beverages mainly occurs in own brand products. Tenwow is seeing a fall in the demand for its own brand alcoholic beverages as the government clamped down on excessive public spending for overseas trips, food and entertainment and public vehicles. Leading Chinese alcoholic companies including Moutai and Wuliangye have seen a reverse in their fortune after spending is curbed.

Top chart is own brand products, while the bottom is third party products. Revenue (RMB m)

Alcoholic beverages continue to contribute the bulk of gross profit despite suffering from shrinking share in terms of revenue contribution. The high gross profit contribution of alcoholic drinks can be explained by the shift towards higher value products.

2013 is the year where non-alcoholic beverages had a stellar performance and this category including RTD tea, herbal tea and energy drink will drive future growth.

% share of gross profit by segment

Conclusion:

Charcoal Roasted Series

Non-alcoholic beverages

Growth opportunities will increasingly come from non-alcoholic beverages. In 2013, Tenwow launched the “Charcoal Roasted Series” milk tea. In 2014, the company will debut “Charcoal Roasted Café Mocha” and “Charcoal Roasted Café Latte”, and cup-milk tea products. Tenwow is still a small player in the milk tea segment, which is now dominated by Master Kong (Tingyi) and Uni-President. The nimbleness of Tenwow makes any increase in sales reflecting strongly in terms of percentage point due to the low base effect.

Tenwow Idea snacks

Food and snacks

The company is betting on mini packaged food and snacks to drive category growth. There are plans to launch more mini products following the success of the Tenwow Idea line.

Alcoholic beverages

The government clampdown on mid to high-end alcoholic drinks shows the need for Tenwow to move into alcopop with low alcoholic content such as Barcadi Breezer to reach the young market.

Good design

Tenwow’s pack designs are contemporary and very eye catchy putting it in good stead to attract young consumers.

Finance cost risk

Gearing has reduced to 5% as at 31 December 2013 compared to 43% in 2012. Tenwow is seeing a rise in financial costs to meet the working needs of the company. Total borrowings at the end of 2013 stood at RMB1.32 billion, up from RMB1 billion with RMB1.23 billion being short term borrowing. Net borrowings (total borrowings less cash and cash equivalent and restricted cash) fell to RMB123 million in 2013 from RMB710.1 million.

Attractive valuation

With a PE of 17 times 2013 earnings, the share price still has some upside opportunities given the rising contribution of the own brand business. The key risks are the termination of existing distribution agreements for third party products and high finance costs. However, valuation will continue to be affected as long as the company continues to depend on third party business.

Charoen Pokphand Foods (CP Foods) has launched Phuket-Style Moo Hong and Stewed Pork Leg crafted with tender Chiva pork. These convenient dishes cater to...

‘Goodday Sebarkan Kebaikan’ campaign garnered over RM29,000 in donations

Kuala Lumpur, 24 June 2021 – Goodday Milk, one of Malaysia’s favourite milk brands since 1968,...

")

{kind=link}

{kind=link}